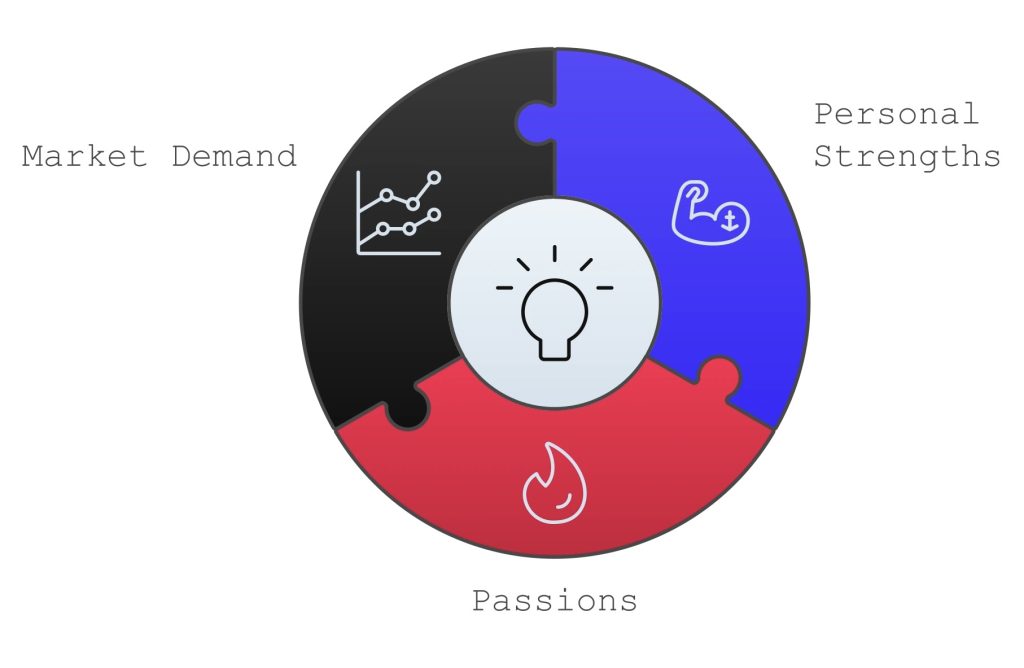

In reality, research findings indicate that 42% of startups fail because of a lack of market demand. Great business ideas must fit what you uniquely bring to the world and meet the market’s needs. So, how do you find that perfect idea? How can you be sure it is just the right idea for them?

Let’s break it down.

Understanding Your Goals and Motivations

Defining Personal Goals

The starting point of a successful business begins with understanding personal objectives. Ask yourself:

- Do you want to be financially independent?

- Do you want more flexibility in your schedule?

- Do you want to create a legacy or make an impact on society?

Clarity of goals will help guide decisions.

Aligning Business Goals with Lifestyle Preferences

Consider how the business will fit into your lifestyle. A very demanding business is out of the question if you want to maintain balance in all aspects of life. Ensure that the goals you set are based on a long-term vision.

| Example: For instance, take the baker Sarah, who desired to start a gluten-free bakery. For a long time, she worked and perfected her recipes, researching the details of the industry. Bringing in a passion for baking with a specific niche, in this case, gluten-free desserts, could channel all energy into making it a mere business and an extension of herself. She was not only a passionate person but also took the business side of learning: from accountancy to customer services; she had the whole recipe that would lead to long-term achievement. |

Evaluating Your Skills and Expertise

Start with Your Passions and Strengths

Your passion fuels perseverance. Think about what excites you or activities you naturally gravitate toward. Whether solving problems, working with people, or creating innovative products, these interests can spark the best ideas. After all, you’ll likely spend countless hours and energy working on it.

Research from Gallup found that entrepreneurs who are deeply passionate about their business are 3.5 times more likely to report a higher level of satisfaction and success. Passion can be contagious—it fuels motivation, helps you push through challenges, and inspires others.

Ikigai and Business Building: Aligning Passion with Purpose

The Japanese concept of Ikigai—”reason for being”—offers a robust framework for building a meaningful business. By integrating what you love, what you’re good at, what the world needs, and what you can be paid for, you can create a business that is not only successful but also deeply fulfilling.

Applying Ikigai to Business

- What You Love (Passion): Focus on an area that excites and motivates you, ensuring you enjoy the entrepreneurship journey.

- What You Are Good At (Skills): Build your business around your talents or expertise to deliver value effectively.

- What the World Needs (Purpose): Identify problems your business can solve or gaps in the market you can fill.

- What You Can Be Paid For (Sustainably): Ensure your idea is financially viable, turning your efforts into a sustainable income.

Benefits of the Ikigai Approach

- Balanced Motivation: Aligning passion with the needs of society and financial goals drives long-term commitment.

- Customer Connection: Conducting a business according to one’s values promotes fulfillment and direction.

- Personal Fulfillment: Running a business aligned with your values enhances satisfaction and purpose.

Apply the principles of Ikigai to create a business with a more significant impact and greater rewards for your entrepreneurial strategies and efforts.

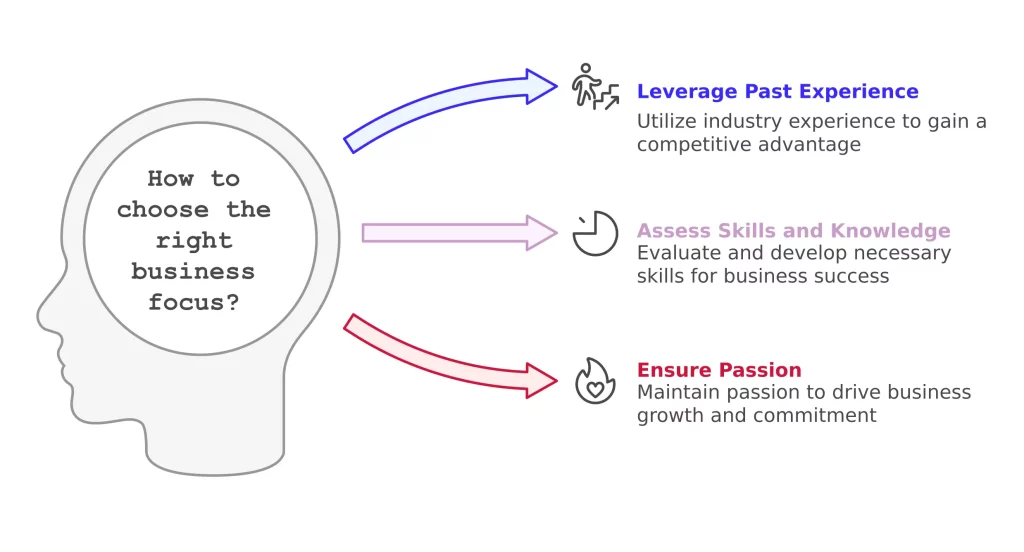

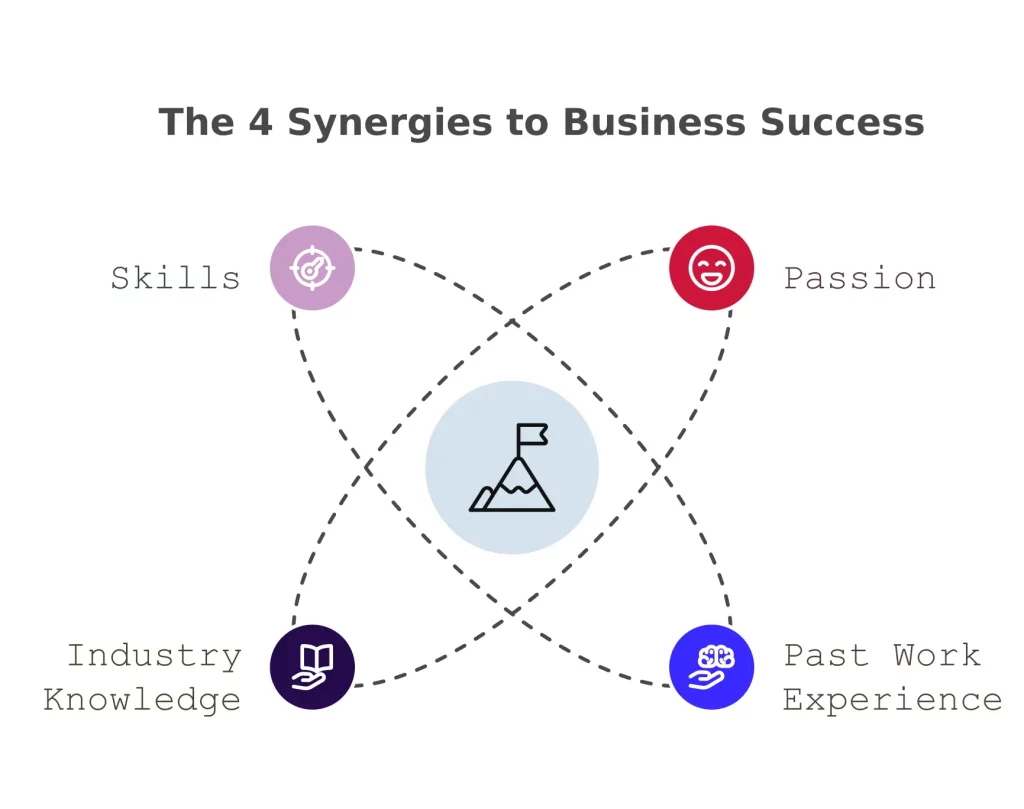

Leveraging Previous Experience

While passion is not enough, your past work experience will explain what business you should focus on. Think about industries or jobs where you excelled so you can determine how to translate these experiences into a venture. Similarly, you must evaluate your skills, knowledge, and experience.

According to a Kauffman Foundation study, 39% of successful entrepreneurs note that prior work experience within the industry was a significant advantage to their success. Ensure you’re passionate and have developed or are willing to develop the necessary skills for your business to flourish.

Conducting a Skills Inventory

Write out your key skills. Technical, creative, and interpersonal skills all count. For instance:

- Do you have expertise in Coding, graphic design, or teaching?

- Do you have world-class networking skills?

Identifying Areas for Growth and Learning

No one is an expert. Identify where your knowledge gaps lie and be prepared to learn. This mindset towards growth can be a gateway to innovative ideas you might not have thought about.

Identify Market Demand and Solve Real Problems

No matter whether your idea is excellent, it won’t succeed without sufficient demand. According to CB Insights, 42% of businesses fail due to a lack of market resources. So, identifying a real problem to solve is key. Look around—what are people struggling with? What gaps can you fill? Niche businesses that solve a specific issue are more likely to thrive.

Analyzing Industry Trends

Keep yourself updated on the latest trends and emerging industries. Use Google Trends, industry reports, and online forums to see what’s gaining traction.

Market Research Tip:

Use tools like Google Trends or social media to observe people looking and talking about. Search for recurrent complaints or unmet needs that consistently appear within specific online communities or forums, such as Reddit. Knowing your target audience’s pain points is the first step to any successful business idea.

Identifying Customer Pain Points

Great business ideas address problems. Ask prospective consumers or online communities about challenges and unfulfilled requirements.

| Example: Imagine being a fitness enthusiast and setting out to start a workout app. Before you can begin to, you ask yourself what problem this does not solve with existing apps. So many apps don’t provide for beginners or those with an injury. In general, one size fits all, and it infuriates the user. Therefore, you launch a fitness app targeting beginners and those with injuries, providing them with personalized, injury-conscious workout plans. Your solution caters to an uncovered market segment or solves the specific problems an underserved group needs to solve. |

Assessing Competitor Offerings

Competition is inevitable in business, but there’s a fine line between too much and too little. Research from Harvard Business Review suggests that startups that enter a market with low competition often fail to meet a real customer need. In contrast, those in crowded markets can differentiate themselves by offering something unique. It’s crucial to study your competitors to see if there’s space for you to stand out.

Analyze the strengths and weaknesses of competitors. What unique value proposition can your idea bring to you that will separate you from others?

| Example: Take, for example, the rise of meal kit services like Blue Apron and HelloFresh. Though the market is competitive, there is still space for differentiation. A new company could focus on a specific dietary need—keto or vegan meals—or promote sustainability by offering fully biodegradable packaging to appeal to eco-conscious consumers. You can carve out your niche by identifying what competitors lack or where they fall short. |

Competitive Research Tip:

Use tools like SEMrush or Ahrefs to analyze competitor websites and see what keywords they’re ranking for. Study customer reviews to find recurring complaints, then position your business as a solution to those pain points.

Evaluate Profit Potential and Scalability

A great business idea should also have significant profit potential and be scalable. According to a report by Small Business Trends, 40% of businesses fail because they can’t scale. So, ask yourself: What are the startup costs? How much do you expect to earn in your first year? What’s the growth potential over the next 5 to 10 years?

Estimating Startup Costs

Determine the financial requirements for your business, including:

- Equipment or inventory

- Office space or virtual platforms

- Marketing and branding expenses

- Software subscriptions needed

Analyzing Revenue Potential

Project approximate earnings of the business. Compare these businesses and search for the corresponding earning potential.

Evaluating Legal and Regulatory Requirements

Research the licensure, permits, and industrial regulations. Non-conformity will result in violations or delays later.

| Example: Let’s assume you are considering a mobile car wash service. On the face of it, this sounds very profitable, but the financials must be evaluated. How much equipment will you have to invest? What is the cost per wash? How many customers will you need to serve to break even? Is there room to scale up with more vehicles or franchising? In contrast, starting an online store selling custom-made T-shirts has lower overhead costs and can be scaled globally with minimal additional resources. According to Statista, the global e-commerce market was valued at $5.7 trillion in 2022 and is expected to grow by 10% annually. This highlights the vast scalability potential of online businesses. |

4 Step Roadmap to Test Your Idea Before Fully Committing

Before starting your new business, it’s essential to validate your idea. According to a U.S. Small Business Administration study, 30% of new businesses fail in the first two years, often due to poor market research or unrealistic expectations. So, test your idea first to see if there’s actual interest.

Creating a Minimum Viable Product (MVP)

Produce an MVP of your product or service to test whether it works. The process helps minimize risks and costs.

Conducting Surveys and Collecting Feedback

Talk to potential customers about their needs and gather feedback on your MVP. You can use platforms such as SurveyMonkey or Google Forms to do this easily.

Running Pilot Programs

Test the business idea first on a small scale before the full launch. This phase will enable you to make adjustments according to real-life feedback.

| Example: Start small by offering the service to friends or by a simple booking page; collect their feedback and invest big-time in equipment and a space for an office. |

Validation Tip:

Start with a minimum viable product (MVP)—the simplest version of your business that still provides value. Use feedback from your first customers to refine your offering before scaling up.

Consider Timing and Market Trends

According to Nielsen’s research, 64% of consumers are willing to pay more for sustainable products. Environmental trends are thus increasing in the world. Hence, success is tied to how business organizations stay on top of changes in new emerging trends and the latest emerging technology.

| Example: Impossible Foods and Beyond Meat took off as the plant-based movement emerged in the light of health and environmental awareness. With the industry booming, it is expected to reach $77.8 billion by 2025. |

Trend Spotting Tip:

Follow industry blogs, attend trade shows, and pay attention to consumer reports. Tools like Google Trends and BuzzSumo can also help you track rising topics in your industry.

Trust Your Gut (But Do Your Research)

Trust your instincts—62% of entrepreneurs cite it for key decisions (Harvard Business Review). Combine instincts with research and data for thoughtful, informed choices.

Understanding Financial Risks

Calculate the risks involved, including potential losses. This clarity ensures you’re prepared for challenges.

Managing Uncertainty

No business is risk-free. Embrace uncertainty with contingency plans and adaptive strategies.

Balancing Short-Term and Long-Term Rewards

Weigh immediate benefits like profitability against long-term growth opportunities. A balanced approach helps sustain your business.

Seeking Mentorship and Advice

A startup business can be daunting; you don’t have to do it alone. Sometimes, seeking the advice of those who have walked that path before will save you time, resources, and effort. Mentorship and advice bring you much knowledge and help you avoid common pitfalls as you build your business.

Connecting with Industry Experts

Another source of knowledge is experts in their fields. Attend networking events, connect on LinkedIn, or join professional organizations.

Joining Entrepreneurial Communities

Entrepreneurship thrives in teamwork. Join forums, coworking spaces, or local meetups to share your ideas and gather support.

Learning from Successful Entrepreneurs

Read biographies of successful entrepreneurs, interview them, or listen to podcasts discussing their successes and mistakes.

Making the Final Decision

After brainstorming, researching, and validating ideas, it is time to select the one that best fits your goals and has the highest potential for success. Making the final decision can feel overwhelming, but by prioritizing, analyzing, and trusting your instincts, you can confidently move forward with your chosen idea.

Prioritizing Business Ideas

Narrow your ideas by weighing their potential against your skills, interests, and market needs.

Using a Decision-Making Framework

Decision-making tools such as SWOT analysis can effectively evaluate ideas systematically.

Trusting Your Instincts

Sometimes, your gut instinct guides you more surely than any other. Trust your instincts to make that final call.

Next Steps After Choosing a Business Idea

The most significant milestone is selecting your business idea, but that’s not where the journey ends. The next most important steps are crucial in bringing the concept to life. They include planning and funding, the initial steps toward creating a support network, the base of a successful launch, and sustainable growth.

Creating a Business Plan

An all-inclusive plan that gives out your goals, strategies, and financial projections. A good plan is a precursor to success.

Securing Funding

Explore funding options, including personal savings, loans, or investors. Another option is the crowdfunding platforms, such as Kickstarter.

Building a Support Network

Surround yourself with a network of mentors, peers, and professionals to help you through challenges.

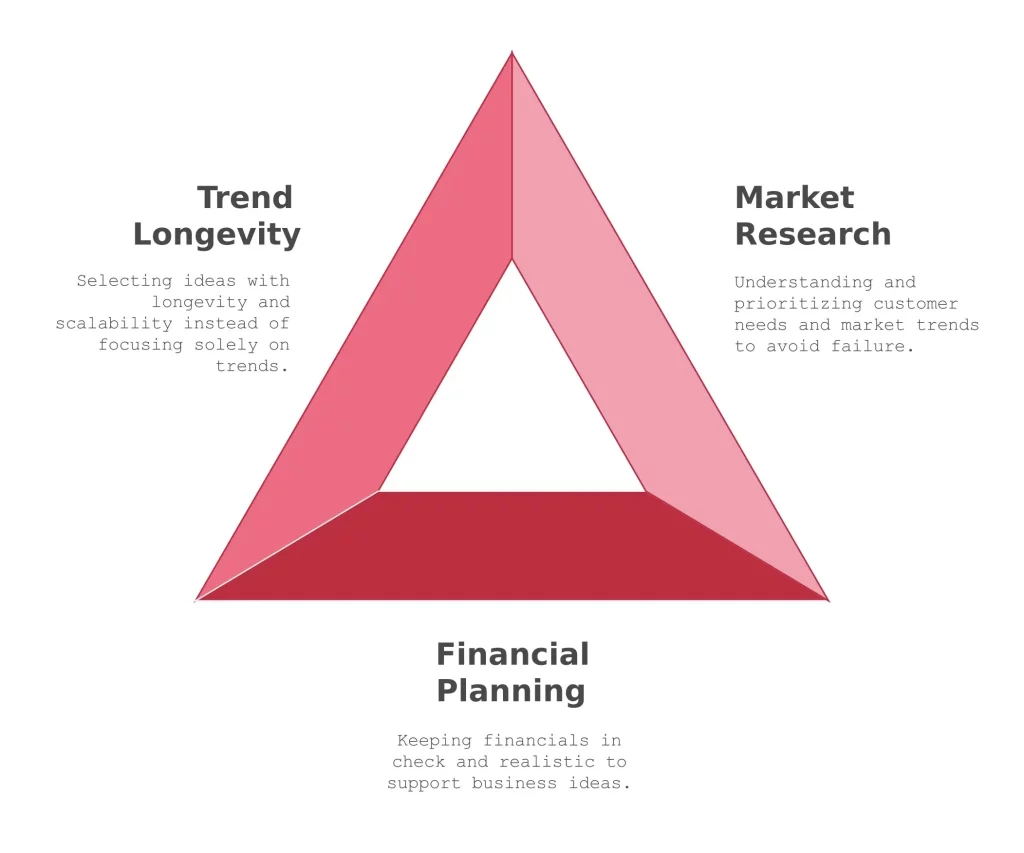

3 Common Mistakes to Avoid

Ignoring Market Research

Overlooking customer needs and market trends can lead to failure. Always prioritize thorough research.

Overlooking Financial Planning

Even good business ideas can get derailed with this lack of budget planning. Keep your financials in check and realistic.

Focusing Solely on Trends

Trends go out of style quickly. Select ideas with longevity and scalability.

Choosing the correct business idea is challenging yet satisfying. Passion, market demand, and profit should be balanced. There is a considerable need for research—75% of entrepreneurs who engaged in market research expanded their businesses within two years (SBA). Start small, validate the idea, and refine it with feedback. Nothing is perfect; however, careful planning and problem-solving increase success. Trust your instincts, research deeply, and confidently get on your entrepreneurial journey!