In fact, while the allure of entrepreneurial success is addicting (yet essential), building a great business requires more than just the initial idea; it demands meticulous planning and consistent execution. Studies reveal that 20% of small businesses fail within the first year, while 50% close within five years (U.S. Bureau of Labor Statistics).

If your conviction has not been determined yet, this step-by-step guide will walk you through all the stages you need to get your startup up and running. Here, you’ll find detailed insights, real-world examples to inspire you, and data to help you navigate the complex but rewarding path to business ownership.

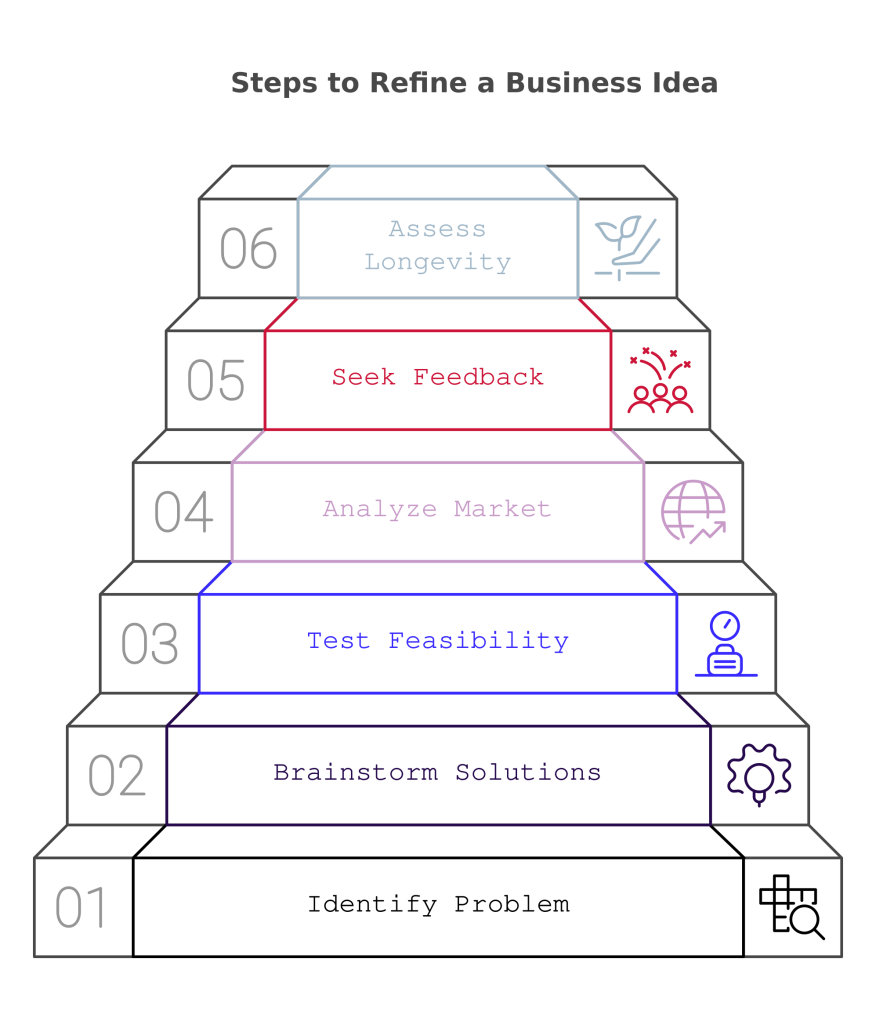

1. Refine Your Business Idea

Your business idea is the foundation of your entrepreneurial journey. It should address three critical aspects: passion, skill, and market demand. An idea that excites you but lacks demand is risky, while a profitable idea that doesn’t align with your interests may lead to burnout.

How to Refine Your Idea:

- Identify a Problem to Solve: Observe pain points in everyday life or work environments. Most successful businesses are the result of filling an unmet need. Reflect on your own experiences or issues you have faced.

- Brainstorm solutions: Write down all possible ways your product or service can address these gaps. Consider how your offering can be faster, cheaper, or better than existing solutions.

- Test feasibility: Evaluate whether your idea is realistic in terms of cost, time, and resources required to execute

- Analyze the Market: Are others addressing the same problem? If so, what unique angle can you bring?

- Seek feedback: Share your concept with trusted friends, industry professionals, or potential customers to refine and validate your idea. Do not begin constructing your building in complete isolation, in detached areas that do not resonate with the marketplace. Remember that negative feedback is beneficial because it helps to find out more significant or even concealed opportunities and threats.

- Assess Longevity: Trends can be fleeting. Use them to ponder whether the idea that you have formed has any longevity or is consistent with the long-term market trends.

| Example: Imagine you’re an avid cyclist frustrated by the lack of eco-friendly bike maintenance kits. By creating a biodegradable product line, you address a growing demand for sustainable options while tapping into your passion. If this is a business you resonate with, consider that the sustainable products market is expected to grow by $150 billion globally by 2030 (Nielsen). |

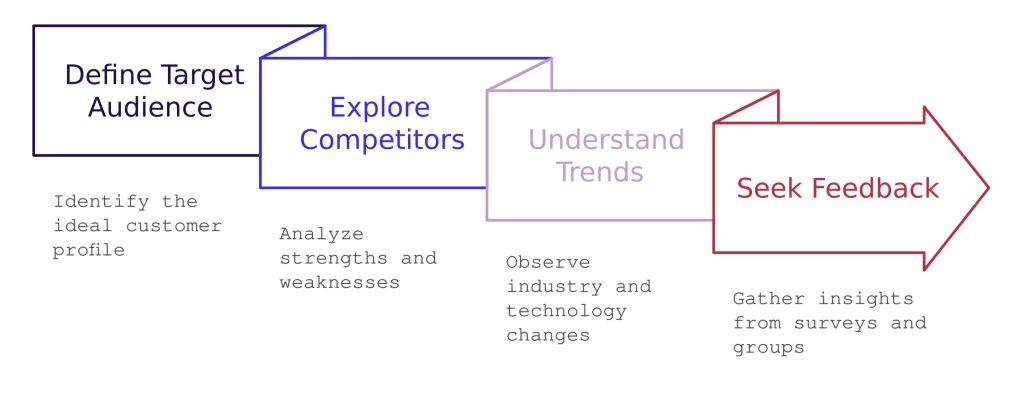

2. Conduct Market Research

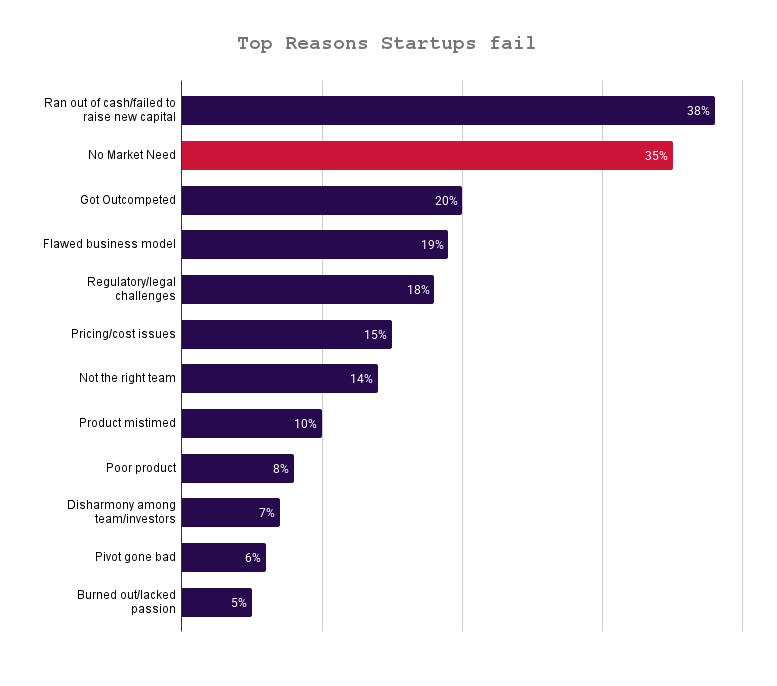

CB Insights reports that 35% of startups fail due to a lack of market fit; in other words, no one cares about your product/service. To avoid this, thorough market research bridges the gap between assumptions and reality. It plays a major role as it assists you to gain a deeper understanding of your audience and your competitors, besides helping you keep an eye on emerging trends within your market. Not only does market research improve the effectiveness of your business plan, but it also helps achieve a better empathic understanding of the intended consumers, clients, and customers.

Steps to Effective Market Research:

- Define Your Target Audience: To whom will you be targeting your product? Who does the service want to appeal to? Define the demographic, psychographic, and behavioral characteristics. Create a detailed persona of your ideal customer/client, including age, gender, income, interests, and buying behaviors.

- Explore Competitors: Analyze your competitors’ strengths, weaknesses, pricing, and marketing strategies. Many competitors’ performances can be easily checked using tools like SEMrush or Ahrefs.

- Understand trends: New changes in the industry, advancements in technology, customer preferences, and demands should be observed. Conduct surveys or check market trends using Google Trends or social media to identify what customers need to exist in the market.

- Seek Feedback: Ask people directly by giving a survey or focus group, review online resources, and check self-reports on any available data to be more complete.

| Example:If you’re launching an online course for aspiring digital marketers, survey professionals to identify skill gaps they’re eager to address. Combine these findings with competitor research to pinpoint your course’s unique selling points (USPs). |

3. Develop a Business Plan

A business plan is your roadmap, outlining your goals and the steps needed to achieve them. Investors and lenders often require one, and it helps clarify your vision. Businesses with a formal plan grow 30% faster than those without one (SBA).

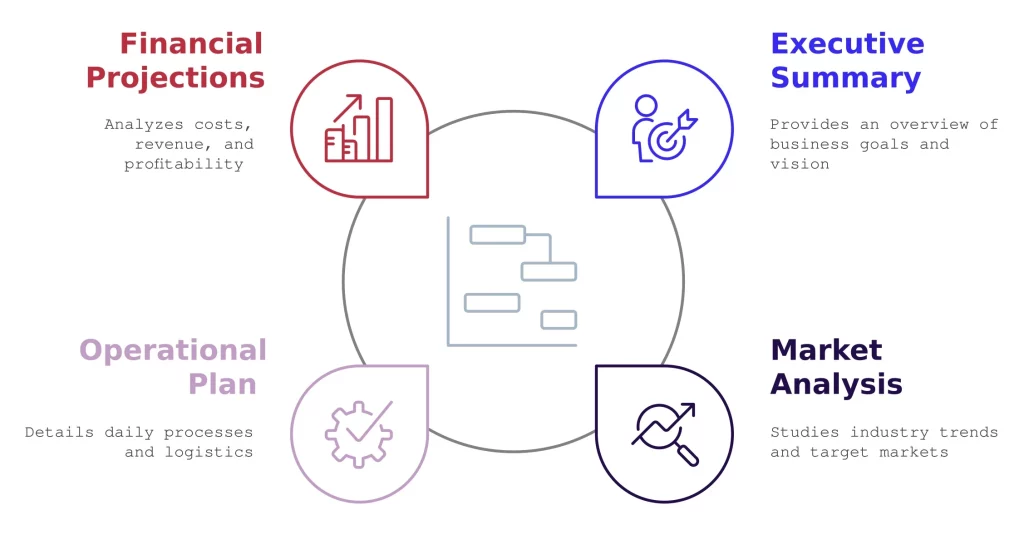

Key Sections:

- Executive Summary: Write a concise overview of the business you want to build. Include a mission and vision statement to clearly present your business’s purpose and long-term goals.

- Market Analysis: Present a thorough study of industry trends and target markets. Use this section to describe how you plan to position your business and make a difference in the marketplace that you have identified.

- Operational Plan: A section breaking down the daily processes, production timelines, supply chains, and logistics.

- Financial Projections: Provide a detailed analysis of the startup costs, revenue projections, cash flow analysis, break-even points, and profitability timelines.

| Financial Projections Example:For a subscription box offering consumable skincare products, include:Projected costs of sourcing and packaging items.Costs related to influencers’ cooperation and other advertisement campaigns.Revenue estimates based on projected churn and subscription tiers.Online store website development costs.Identify the SAAS tools, such as e-commerce platforms like Shopify, CRM like Hubspot, etc, that will enable you to run your business. |

4. Choose the Right Business Structure

Your business structure determines legal liabilities, the tax regime followed, and any business entity’s distribution of profits or losses. Make sure you choose the business structure that best fits your strategy and vision.

Common Structures:

- Sole Proprietorship: Easiest to setup; however, they don’t offer any protection of the liabilities.

- Partnership: Shared responsibilities and profits; ensure a solid partnership agreement. Partnerships are mainly set up for the provision of traditionally professional services, such as legal and accounting firms.

- LLC (Limited Liability Company): Protects personal assets and offers flexible taxation. Prominently, it affords a way to avoid or minimize individual responsibility, tax, and control over the operations.

- Corporation: A separate legal entity ideal for businesses seeking investors but comes with regulatory complexities.

Let’s break down the Pros and Cons for each. See which one fits you most:

| Business Structure | Pros | Cons |

| Sole Proprietorship | – Simple and inexpensive to set up.- Full control over decisions.- Minimal regulatory requirements. | – No liability protection; personal assets are at risk.- Limited ability to raise capital.- Difficult to scale beyond a small business. |

| Partnership | – Shared skills and resources.- Simple and low-cost setup.- Shared financial load.- Flexible management.- Tax advantages.- Boosts credibility. | – Shared liability risks personal assets.- Potential conflicts over decisions and profits.- One partner’s actions impact all.- Limited lifespan without proper agreements.- Unequal profit sharing can cause disputes. |

| LLC (Limited Liability Company) | – Protects personal assets from business debts.- Flexible taxation options (pass-through or corporate tax).- Easier to manage than a corporation. | – Can be more expensive to set up compared to a sole proprietorship.- Additional paperwork for compliance.- Self-employment taxes may apply. |

| Corporation | – Strong liability protection for owners.- Easier to attract investors and raise capital.- Perpetual existence, even if ownership changes. | – More complex to set up and manage.- Subject to double taxation (C-Corp) unless electing S-Corp status.- Requires strict compliance with regulations and formalities. |

| Example:A freelance graphic designer starts a freelance graphic design business as a sole proprietor, keeping things simple and cost-effective. As the business grows and attracts larger clients, she transitions to an LLC to protect her assets and present a more professional image. Later, with plans to scale and attract investors, the freelancer converts the LLC into a Corporation, allowing the option to issue shares and formalize corporate governance. Each transition aligns with the business’s evolving needs and goals. |

5. Register Your Business

After settling for the type of business most appropriate for your startup, it is crucial to proceed with the correct business registration to conform to the law. Steps include:

- Choose a business name: Ensure it sets yourself or your brand apart from your competitors and aligns with your organization’s values. We recommend also checking domain availability. Get your website domain name search here.

- File necessary paperwork: Register with your state or country. Deep research and speaking to your local Financial advisor would be highly advised. For U.S. businesses, check with your Secretary of State’s office.

- Obtain an EIN: Apply for an Employer Identification Number from the Inland Revenue if you hire employees or operate as an LLC or corporation.

- Check licensing requirements: Depending on your industry (e.g., food service, construction), you may need local, state, or federal permits.

- Apply for VAT certification: Once you have registered your business, you should be able to apply for your Value Added Tax Certification if this applies. Especially if you are planning to sell goods or services.

6. Secure Funding

Financial resources are the lifeline of any business. Estimate your startup costs and explore funding options, which may vary based on your industry and business model.

Startup costs vary greatly, so identifying the right funding source is crucial. Consider these avenues:

Common Funding Sources:

- Bootstrapping: Use your savings to control your business entirely, but manage cash flow cautiously.

- Loans: Small business loans can provide needed capital. Prepare detailed financial statements and a solid business plan to secure approval.

- Crowdfunding: Platforms like Kickstarter allow you to raise funds while building an audience.

- Investors: Angel investors or venture capitalists exchange funding for equity. These investors can provide significant funds but may expect equity in return.

- Grants and competitions: Research local or industry-specific grants for small businesses or participate in pitch competitions.

| Example:An online tutoring platform would begin with bootstrapping to create its website and initial courses. A small business loan would then be used for upgrading, while crowdfunding can help launch new features and build a community of learners. After a couple of years in business, scaling up would be supported by angel investors or venture capitalists to provide equity funding and cover extra costs; educational grants or pitch competitions can also be helpful. |

7. Build Your Online Brand

A digital presence is non-negotiable in today’s market. Hubspot and Google claim that 81% of shoppers research online before purchasing. Your website and social media channels are your business’s storefront, especially for e-commerce ventures.

Key Steps:

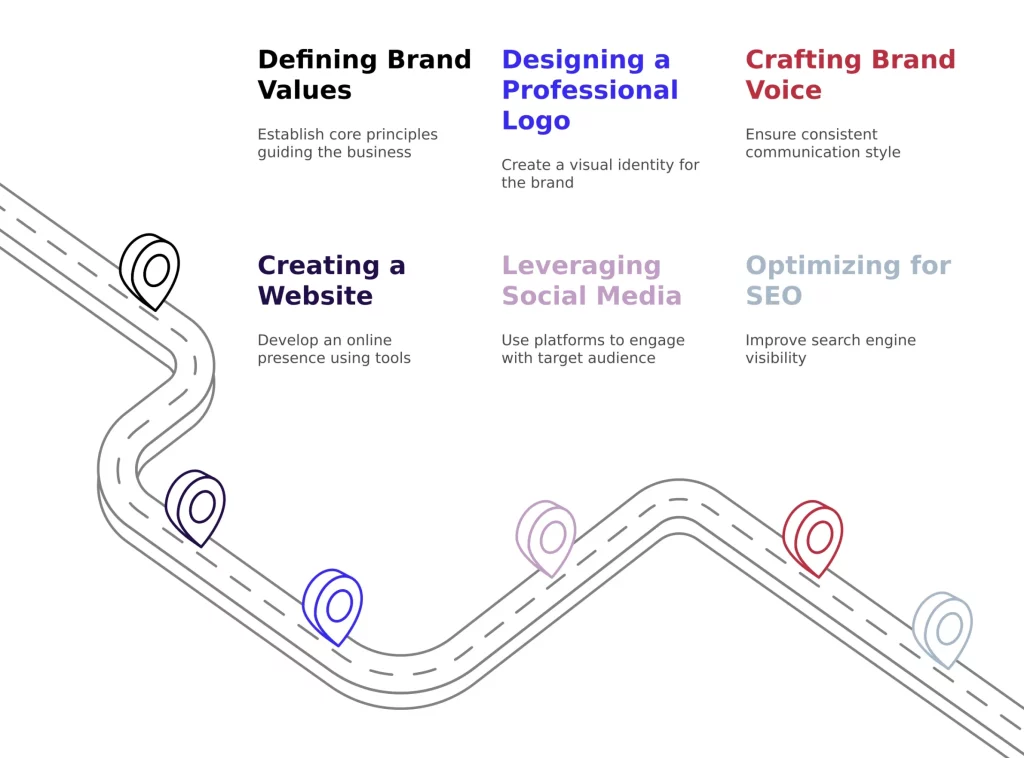

- Defining brand values: Establish the core principles that guide your business, such as sustainability or innovation.

- Designing a professional logo: Work with experienced designers or use platforms like Upwork and Fiverr to find your designer. You can use tools like Canva and 99design to create it yourself.

- Crafting your brand voice: Whether formal or casual, ensure consistency across marketing channels.

- Create a Website: Platforms like Wix or Shopify are beginner-friendly and can be used to fast-track your launch. Otherwise, you can hire a developer on a project-basis to help you build the site.

- Leverage Social Media: Use Instagram for visual businesses and LinkedIn for B2B services or to sell products online.

- Optimize for SEO: Research keywords to rank higher on search engines.

Engage with customers through regular blogs, social media, and newsletters to strengthen your brand connection.

| Example:A game developer focuses on creativity and game dynamics, appealing to 73% of gamers who value engaging content. They designed a bold logo with Canva, launched a website using Shopify to boost conversions by 35%, and used social media like Twitter and Discord to connect with 80% of gamers active online. SEO optimization and engaging blogs about game updates attract 53% organic traffic, while personalized newsletters keep 61% of their audience engaged. |

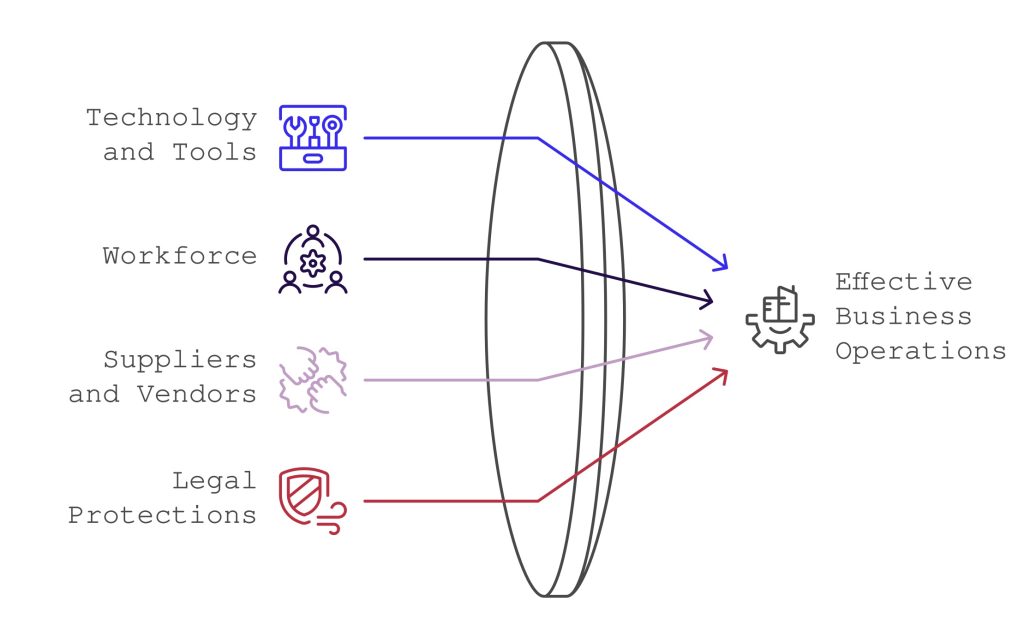

8. Set Up Operations

Effective operations ensure seamless delivery of your product or service. Address the following in detail:

- Technology and tools: Invest in inventory, project management, and accounting software.

- Workforce: Develop clear job descriptions and provide training for new hires. If working solo, define your daily routines.

- Suppliers and vendors: Build strong relationships with reliable suppliers to avoid disruptions.

- Legal protections: Draft contracts, NDAs, and other agreements to safeguard your business interests.

Operational efficiency often determines customer satisfaction and profitability.

9. Test Your Idea Before Fully Launching

Validating your business idea before a full launch minimizes risk, saves resources, and ensures your offering resonates with your target audience.

Steps to Validate:

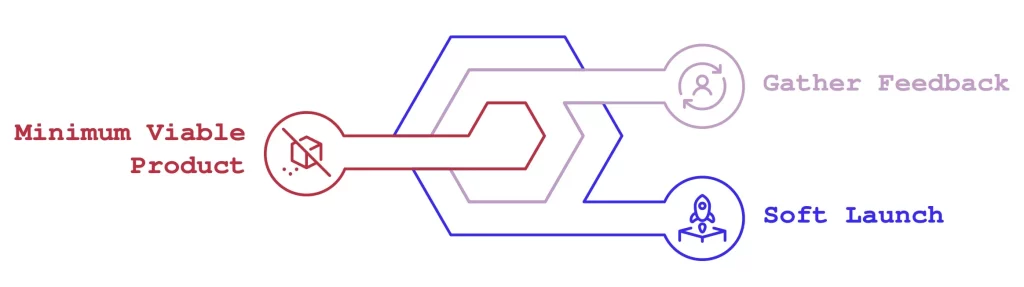

- Create an MVP (Minimum Viable Product): Develop a simplified version of your product or service, focusing on core features to test market interest. In other words, introduce a basic app version or limited product line.

- Gather Feedback: Conduct social media polls, focus groups, or surveys to understand the customers’ preferences, pain points, and expectations. It can be done with the help of tools such as SurveyMonkey or Instagram polls.

- Soft Launch or Beta Test: Roll out your product to a small group of users and test it in real-life conditions. Monitor their behavior and collect feedback on where it needs improvement.

Key Tools: Prototyping tools Figma, Google Forms for creating surveys Google Analytics or Hotjar to monitor behavior during beta tests Refine your idea based on feedback from this testing to guarantee a successful full launch.

| Example:A clothing line might start with a limited release of one product. Customer reviews would enable them to hone appropriate designs. This further increases exclusivity, and the potential customers do not have to be lost in the multitude of choices. |

10. Launch and Monitor Performance

Your launch should be an event to create awareness of the product, and this should be planned carefully. Consider a soft launch, a limited release to test and gather feedback, and helps deploy funds into a better hard launch strategy – whereas the latter is a full-scale release with significant marketing efforts.

During operation, use analytics to compare with your metrics and your customers’ feedback to adapt.

Key Launch Tips:

- Offer promotions or discounts for early adopters.

- Use email marketing and social media ads to drive traffic. A tip on emails: Email marketing offers an ROI of 4,400%—one of the most effective channels for startups (DMA), while social media ads expedite your reach quickly to a granularly defined audience.

- Track key metrics: Monitor sales, website traffic, and customer retention rates. Use tools like Hub Spot or Google Analytics for insights.

- Gather customer feedback: Surveys, reviews, and direct contact with customers will help understand their preferences and improvements.

- Adapt to market trends: Keep updated on technological developments and consumer behavior to maintain competition.

- Revisit your business plan: Change your goals and strategies as your business changes.

Remember, long-term growth would be sustained by adaptability in a dynamic business environment.

| Example:A meal delivery startup launches with an early adopter 20% discount, using high-ROI email marketing and targeted social media ads to drive traffic, monitoring sales and retention in Google Analytics, soliciting feedback through surveys, and changing food trends by keeping up with them in terms of updating their business plan. |

Starting a business is an ambitious but achievable endeavor if approached with the right strategies. Each step is a building block for long-term success, from refining your idea to launching and scaling. By combining passion, preparation, and adaptability, you’ll set yourself apart from competitors and increase your chances of thriving in the entrepreneurial world.